- Q1 22 Revenues 88.4 Cr vs Q1 23 106.8 Cr – Decline of 17%

- EBITDA 15.2 Cr vs 26.3 Cr – Decline of 42%

- EBITDA % at 17% vs 25%

- Geopolitical issues, covid lockdowns in china and semiconductor shortages affected the company’s performance

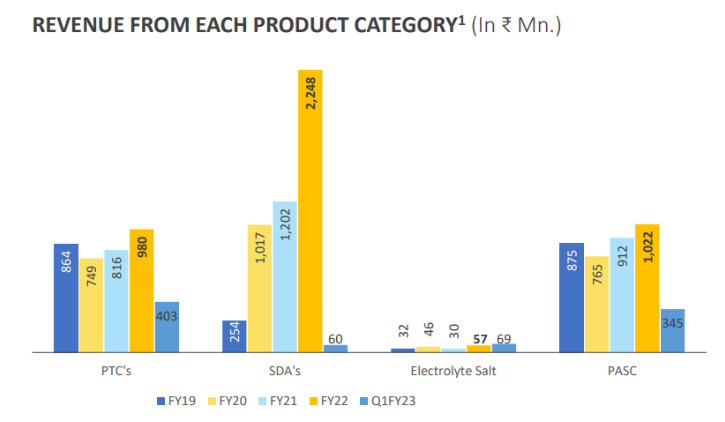

- Q1 22 – 52% vs 7% Q1 23 – SDA Contribution

- Forex loss of 4.9 Cr. Actual EBITDA = 20.17 Cr. EBITDA margins 23%

- SDA is high margin product

- Application of zinc ion and sodium ion batteries is increasing.

- Received the formal approval from the customer for energy storage application and manufacturing started. Working with 2 more customers for the electrolyte salts segment.

- Monoglyme : Pilot stage equipment using continuous flow chemistry will be installed in Q2 23.

- Another product pilot equipment is already set up and trials are going on. Commercial supply will take 15-18 months.

- New product in application of metal extraction has been formally approved by the customer and commercial supply will start from Q4 FY 23

- Expecting Good revival form Q4 Fy 23 for SDA

- New Application of SDA based Zeolite catalyst is into recycling of waste. Tatva Chintan developed the SDA for this application

- Flame retardants : Successfully completed pilot plant trials. Necessary infra installed at plant scale & full scale production to begin from this week

- There was a strike for construction material in Gujarat for 3 weeks, despite that it is expected to start the plant according to schedule in Q3 FY 23.

- Customers are not buying SDAs because of drop in demand and inventories are high.

- From Q4 23 demand will normalize for SDAs. Maximum 10% drop of SDAs for full year of FY 23.

- Since tatva chintan is not able to sell SDAs they are manufacturing more PTCs and selling them in the market. Added MNC customer from Europe and captured 80% of their volume.

- Global market size of flame retardants is 150000 MT while tatva chintan is planning to set up the plant of 5000 MT. There is no competitor for flame retardants in India. Global competitors are Lanxess, ICL, Albemarle

- Adding 200 KL capacity, doubling the existing capacity. Revenues are expected to double after addition of new capex.

- Metal extraction product revenue potential : 30 to 40 Cr

- Register for model portfolio to get detailed analysis of various businesses.