The US is the largest Healthcare market in the world. Drugs manufactured by Indian pharma companies account for a significant amount of the prescriptions filled in the US. But the big Indian players in the US market have not been able to drive significant returns for the past few years. Let us try to understand why:

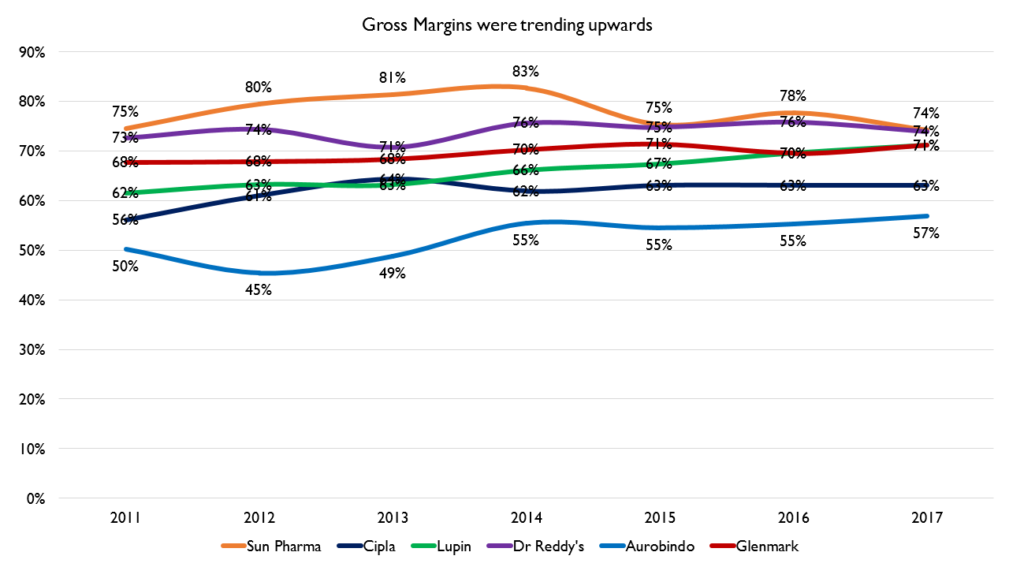

Period of Rapid Growth (FY11-FY17)

During 2010 to 2017, Indian pharma companies saw a boom in the US business. Some of the reasons for this were:

- Lowest cost producer: Indian pharma companies were able to manufacture and sell drugs at very low costs due availability of cheap raw materials from China and availability of cheap labor. These companies gained massive scale and became incredibly efficient at manufacturing low cost medicines.

- Blockbuster drugs going off patent: Between 2012 and 2016, drugs with cumulative annual sales of approximately $100 billion went off patent. The Indian pharma companies were quick to cash in on this and were able to gain significant market share due to their low costs.

- Fewer regulatory issues: At the time, the US FDA did not have the resources to conduct extensive plant audits. As a result, the companies were able to get away with not maintaining the manufacturing plants as per the standards.

- Less Competition: Another side effect of the US FDA being short staffed was that they were not able to clear the backlog of ANDAs and more ANDAs kept piling up. As a result, fewer generic drugs were approved which resulted in less competition. The players that were already in the market enjoyed long periods with no price erosion.

- Fragmented buy side: At the time, there were over a dozen PBMs, who operated independently from insurance providers and hence had lesser power to negotiate lower prices with pharma companies.

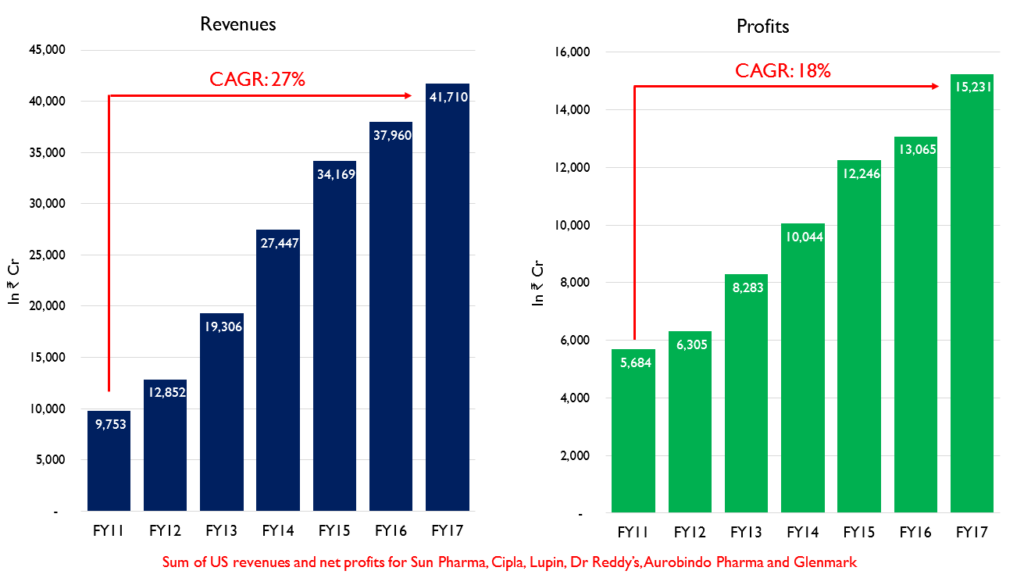

Due to a combination of these factors, Indian pharma companies saw a period of rising revenues and surging profits. Revenues of the top Indian pharma companies grew at a CAGR of 27% during this period and profits grew by a CAGR of 18%.

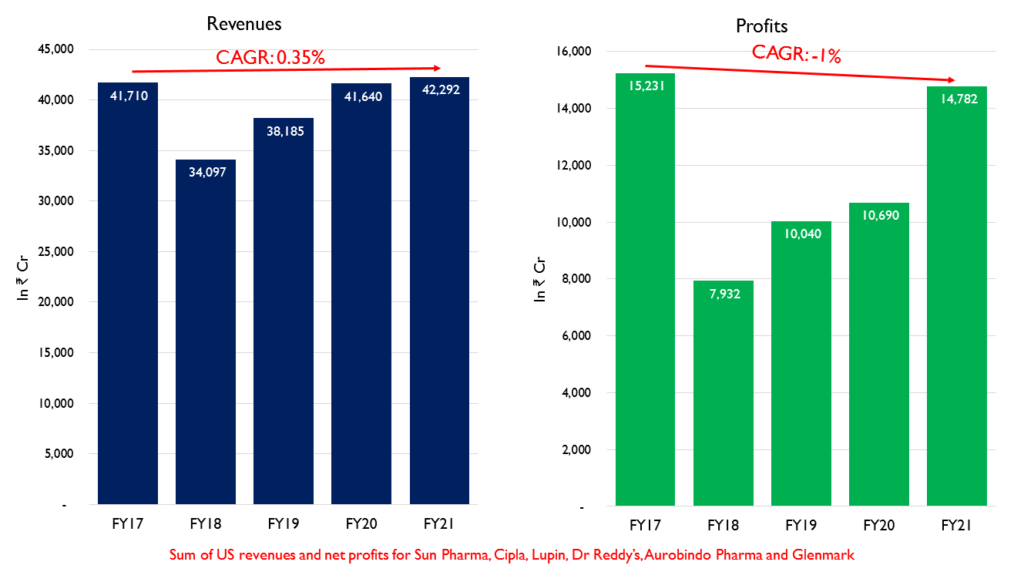

Period of Consolidation (FY17 to present)

By 2017, the Indian companies had built massive scale due to all the factors mentioned above that were in their favor. But the business landscape changed dramatically post 2017, making it hard for companies to enjoy the same level of profitability. Some of the factors that were key to this downturn were:

- Increased costs: The implementation of Generic Drug User Fee Act (GDUFA) added additional costs to generic drug manufacturers. GDUFA fees are collected by the US FDA as a way to solve their lack of funding and manpower. Generic drug companies have to pay a fee for approval of ANDAs and a fee for every US FDA manufacturing facility they have. This added to the costs of selling drugs in the US.

- Increased competition: One of the stipulations under GDUFA was that the US FDA would clear the backlog of ANDAs and also approve ANDAs faster. As the US FDA cleared the backlog of ANDAs, the competition in molecules increased rapidly causing massive price erosion. It is now much easier for new competition to enter into a molecule.

- Increased regulatory requirements: GDUFA fees also enabled the US FDA to hire more manpower to conduct plant audits. They found massive violations at Indian plants and started issuing warning letters. In 2019, 46% of the warning letters issued by the US FDA were to Indian companies. Plant shutdowns led to idle costs and decreasing profitability for these companies.

- Volatile raw material costs: After a massive explosion in a chemical factory in China, the Chinese authorities started shutting down a lot of the API plants. This led to increased raw material costs for Indian formulation companies.

- Consolidation on buy side: There were massive M&As on the buy side which led to consolidation in the drug purchasing side in the US. PBM’s merged with insurance companies and pharmacy chains to vertically integrate their operations. There were about a dozen PBMs in the US prior to 2012 which later consolidated to mainly 3 big companies who control 90% of the drug buying in the US. This gave them massive negotiating power to lower drug prices.

So pharma companies faced the pressure on revenues from increased competition and consolidation and on costs by increased US FDA expenses and volatile raw materials. This has led to a period of decreased revenues and profitability where the combined profit for these firms is still not above FY17 levels.

The Future

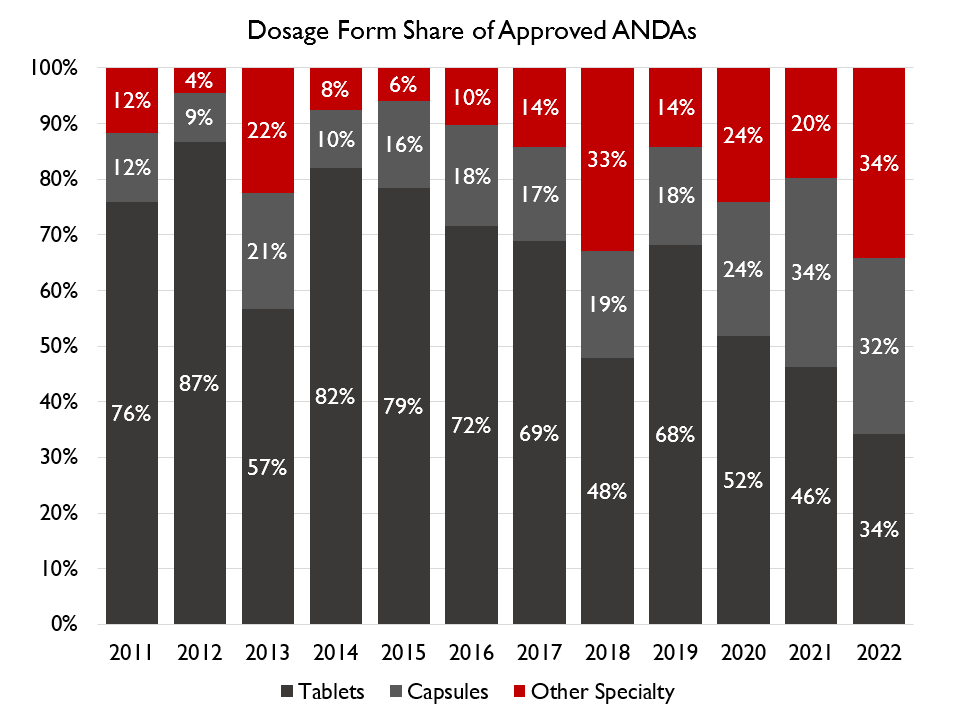

There is most competition in oral solid dosage forms (tablets and capsules) as they are the easiest to manufacture. Their share in the overall product approvals has been decreasing in the past few years as Indian companies are focusing on other complex to manufacture dosage forms like injectable, solutions, gels, powders, lozenges, etc.

The next phase of growth for these companies is expected to come from complex generics, specialty generics and biosimilars. The R&D expenses and time required on these products are much higher. These products are under development and as they start receiving approvals, these companies are expected to deliver another leg of growth.